Author: Melina Scheuber

– 37% Retirement Pension

Despite working similar weekly hours as men, women receive, on average, about 37% or CHF 20,000 less in pension benefits in their old age. While men’s average total annual pension is CHF 52,755, women’s is CHF 33,169 1, 2.

This disparity is largely due to factors like wage inequality, a higher prevalence of part-time work among women, maternity-related work absences, and a greater share of household and family responsibilities 3.

In Switzerland, approximately 60% of women are employed part-time 4,primarily due to domestic responsibilities, especially childcare 5.

Many Swiss women prefer part-time work as it’s challenging to balance a full-time job with family duties. Factors like negative tax incentives for secondary incomes, lower wages, and societal role expectations also influence this choice.

The financial repercussions of opting for part-time work or extended career breaks, including income and pension gaps, are often overlooked. Reduced paid work leads to lower salaries and consequently, diminished pension contributions. Insufficient contributions to the AHV and pension fund (2nd pillar) result in reduced retirement pensions and social security benefits. For instance, each missing AHV contribution year can decrease the pension by 2.27%. A minimum income of CHF 21,510 (as of 2022) is necessary to join a pension fund. Additionally, the coordination deduction adversely affects part-time workers.

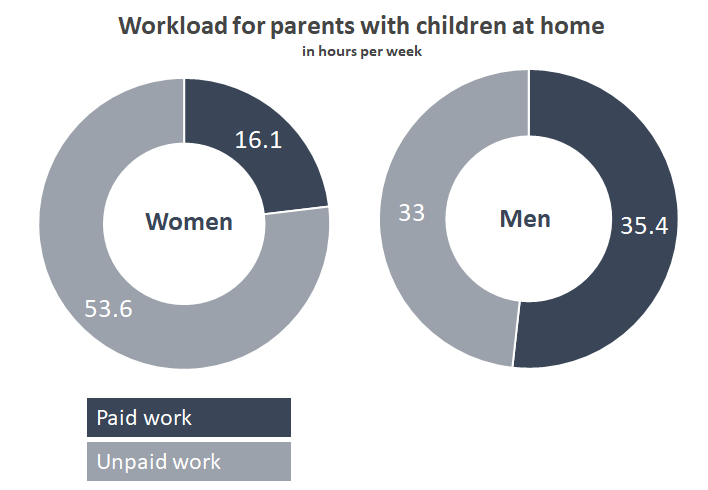

The average employment level for Swiss women working part-time is 50% 5. The Swiss Conference of Gender Equality Delegates (SKG) advises maintaining a workload of at least 70% in the long run to avoid pension cuts6. Working only 40% or 50% for an extended period can lead to significant gaps in occupational pension provision.

Making the Right Provisions to Minimize and Close Pension Gaps

To avoid financial surprises in old age, mitigate risks, and ensure adequate financial security, it’s crucial to examine your financial situation closely.

Where to Start?

Build Financial Knowledge

Money is a daily concern that persists throughout life. It’s crucial to dedicate time to understanding finances. Allocate at least 30 minutes a day to learning, whether it be through sports, cooking, folding laundry, listening to financial podcasts instead of browsing social media, attending online webinars, or reading finance blogs on your commute.

You don’t need to become a financial expert, but acquiring basic financial knowledge is essential.

Regulary Review your Financial Situation

Consider your goals and current circumstances. Are you expecting a child and unsure of the financial impact? Are you considering a job change, thinking about self-employment, or planning to buy a home?

Define your goals and plan accordingly. Financial advisors can guide you in your financial journey. Regularly reassess your financial situation to ensure your personal financial plan aligns with your life situation and goals.

Start Investing

Pillar 3a is a key strategy for preventing gaps in occupational pension provision and saving for retirement. Its restricted access until retirement age, with some exceptions, makes it an ideal platform for securities investments. The long-term nature of these investments reduces the risk of losses and enhances potential returns.

Begin contributing to pillar 3a at a young age. Even if you can’t contribute the maximum amount of CHF 6,883 (as of 2022), smaller monthly amounts like CHF 100 can benefit from compound interest. Regular contributions are important. If contributions are financially challenging, consider working with your partner to find a feasible solution. Couples have the advantage of doubling the tax benefits of pillar 3a.

Fund savings plans or individual investment solutions are additional means to save for retirement, especially if you have savings beyond your pillar 3a contributions.

Take Control of Your Finances Today

How does this resonate with you?

Would you like to be informed once Melina Scheuber or her colleagues publish articles around pension fund and financial topics ?

Please sign up for our newsletter.

You are currently viewing a placeholder content from HubSpot. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More Information

1 Large Difference Between the Pension Amounts of Men and Women

2 Study on the Gender Pension Gap in Switzerland

4 FSO: Part-time Work in Switzerland