Author: Melina Scheuber

A recent study by BNY Mellon Investment Management revealed that Swiss women believe they need a monthly income of over CHF 5,000 to invest in the stock market [1].

Additionally, 40% of Swiss women perceive investing in the securities market as too risky. A notable 54% feel they cannot afford to incur losses from investments [2].

Conversely, women excel in saving, with 79% regularly setting aside money [3]. They prefer savings accounts, considering them secure and easily accessible.

However, this perceived security is misleading. Savings are not subject to the price fluctuations of investments, but due to inflation and low-interest rates, the value of money in savings accounts is effectively diminishing.

Inflation Leads to Currency Devaluation and Wealth Loss

We save money intending to preserve its value. Therefore, the goal of any investment, whether in savings accounts or other forms, is to at least offset inflation with generated income (interest/dividends), thereby safeguarding assets from purchasing power devaluation.

Inflation is essentially a rise in average price levels, leading to money losing value. This is particularly evident in everyday purchases. For example, Migros raised the price of 500 grams of espresso from CHF 4.90 to CHF 5.40 in January 2022, and bread prices have increased by 10 – 15 percent [4].

Leaving money in a savings account results in the very scenario we aim to avoid: a continuous decline in the money’s value and reduced purchasing power. This effect becomes significant with larger amounts, as illustrated below.

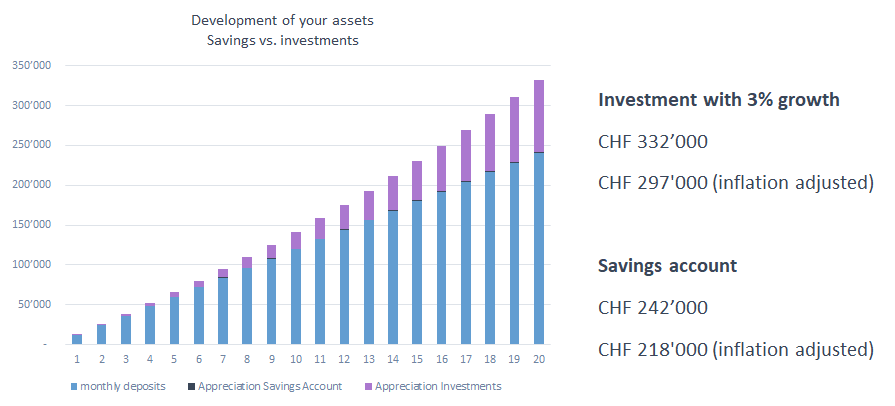

Suppose you deposit CHF 1,000 monthly into a savings account starting at age 40, with a 0.075% interest rate, 1% inflation, over 20 years. At 60, you’ll have saved CHF 240,000, earning about CHF 2,000 in interest, totaling CHF 242,000. However, considering inflation, the purchasing power of your savings would be only CHF 218,000—a CHF 24,000 loss in value.

Withdrawal Conditions Restrict Access to Money

An often-overlooked aspect of savings accounts is withdrawal limits imposed by banks, ranging from CHF 10,000 to CHF 50,000 per year. Exceeding this limit requires planning three months ahead or incurring penalty interest of 0.5% to 2%, depending on the bank.

The Effect of Investing

While savings accounts are stable, they don’t increase in value, and over time, lose worth due to inflation. Contrary to popular belief, keeping money in a savings account is not entirely risk-free. Like investing, it carries its own set of risks.

To financially safeguard yourself, proactive measures are necessary. Just as physical health is maintained through exercise, healthy eating, and occasional massages, financial fitness requires similar attention.

Why Financial Management is Crucially Important for Women

Many associate the securities market with the risk and anxiety of losing money. The fear is that investments might depreciate exactly when you need to access them. Understandably, losing hard-earned money is a concern. Do you share this sentiment? Interestingly, our daily lives are filled with risks – slipping in the shower, accidents while driving, burns during cooking, sports injuries, and so on.

Every day, you decide the level of risk you’re willing to take. The same applies to investing. You can choose the level of financial risk you’re comfortable with. Remember, even savings accounts are not without risk.

Let’s compare a savings account with securities market investments, starting at age 40 with monthly investments of CHF 1,000 for 20 years, assuming a 3.0% annual return after costs (representing a moderate investment strategy) and 1% inflation, against a 0.075% interest rate on the savings account.

With this investment strategy, it’s highly probable you’ll have CHF 332,000 at age 60. Adjusted for inflation, this is about CHF 79,000 more than if the money had remained in a savings account. Yes, investments face price fluctuations and risks over these 20 years. However, long-term capital market investments are generally beneficial.

Life is full of risk-related decisions. The question is, which risks are you willing to take? Is it the long-term fluctuation risk of investments, with a high likelihood of retaining and potentially increasing value, or the high probability of your money devaluing by the term’s end?

Take Control of Your Finances Today

How does this resonate with you?

Would you like to be informed once Melina Scheuber or her colleagues publish articles around pension fund and financial topics ?

Please sign up for our newsletter.

You are currently viewing a placeholder content from HubSpot. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More Information

[1] BNY Mellon Investment Management: It’s time to create a more inclusive investment world

[2] Höchste Zeit für mehr Inklusion am Finanzmarkt | News | Aktuell | investrends.ch

[3] Studie JPMAM_Frauen und Geldanlage 2021 – Für die Zukunft planen (jpmorgan.com)

[4] Gestiegene Rohstoffpreise – Migros und Coop erhöhen die Kaffeepreise – News – SRF