Author: Melina Scheuber

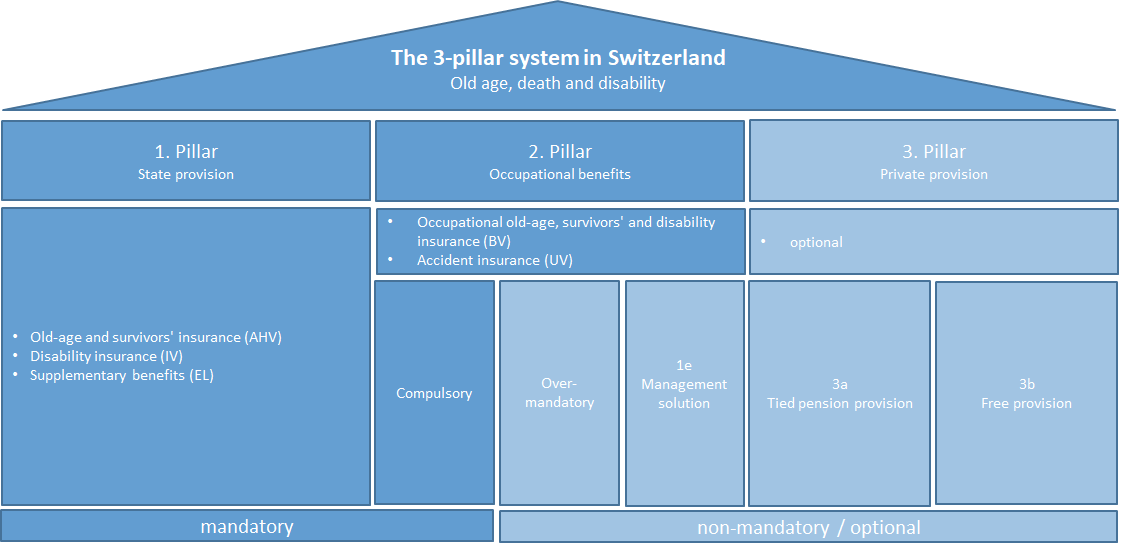

Our pension system relies on three pillars: state, occupational, and private pension provision. Each of these pillars comprises both a pension insurance and a risk insurance component. This means that upon retirement, you receive a pension, and in the case of a risk event (like death or disability due to accident or illness), you, your spouse, and your children are entitled to certain cash benefits. Regarding the 1st and 2nd pillar insurances, cohabiting individuals are at a disadvantage compared to married couples.

Contributions for the 1st and 2nd pillars are deducted from your gross salary monthly and transferred directly to the pension funds by your employer. The amount you receive in your account is your net salary. The 3rd pillar, private pension provision, is optional. You can choose how much and how often you contribute to the maximum allowed amount.

The 1st pillar is designed to secure your basic livelihood, ensuring you can financially survive. Your current contributions fund the benefits of active pensioners, meaning you don’t directly save for your own retirement.

In contrast, the 2nd pillar aims to maintain your standard of living post-retirement and in the event of a risk. Every franc saved in your 2nd pillar is yours in old age.

Most Swiss people prioritize the 1st pillar, often not considering pension fund assets as part of their own wealth. Despite this, a majority have most of their savings in the 2nd pillar. Yet, only 18% of the working population is aware of their own BVG pension capital amount. Furthermore, 50% mistakenly believe their monthly salary deductions are taxes and fees, though these are investments in their retirement capital[1].

It’s crucial to understand that you have significant control over your retirement savings, especially in the 2nd pillar. Choices like selecting an employer, adjusting your workload, or leaving a company directly influence your retirement capital and risk coverage.

Your Influence in the 1st and 3rd Pillars

Pillar 1 – AHV/IV

Your influence over 1st pillar benefits is minimal. However, your retirement pension amount depends on your contribution years and average annual salary. For a full individual pension, you must have contributed to the AHV/IV for 43 years (women) or 44 years (men) without gaps, and your average annual income should be at least CHF 86,040*. Missing contribution years reduce your pension by 2.27% per year.

Pillar 3 – Private Pension Provision

You have considerable influence over 3rd pillar benefits, as you decide your annual contribution. This pillar is ideal for filling gaps in your occupational pension provision and saving for retirement with tax benefits. Comparing provider costs and considering investment in securities are important due to the long-term horizon, which lowers loss risks and increases potential returns.

Your Influence in the 2nd Pillar

Your influence on 2nd pillar benefits is significant, though less direct. In the pension fund, we differentiate between the mandatory part (salaries up to CHF 86,040) and the extra-mandatory part (salaries over CHF 86,040). Mandatory benefits are legally regulated and uniform across pension funds and employers. However, differences exist in the non-mandatory part, where employers choose the pension and insurance benefits for their employees. These can vary across different pension plans.

Example:

Pension Plan 1: Commercial employees, assistants, customer advisors, marketing employees, salaries up to CHF 100,000.

Pension Plan 2: Managers, team leaders, regional heads, salaries up to CHF 200,000.

Pension Plan 3: Management personnel, CEO, CFO, salaries of CHF 200,000 or more.

Benefits vary depending on the plan. This means your benefits from the pension fund depend on your employer, position, and salary level. You could save significantly more retirement capital with one employer over another or receive better risk event coverage for you and your family.

What Can You Influence, When, How, and What Should You Pay Attention To?

Job Change

When interviewing for a new job, discuss not only salary but also pension fund benefits. Comparing benefits among potential employers is key. If you need more information on this topic or require assistance, consider consulting a specialist.

Further opportunities regarding pension assets arising from job changes are detailed here.

Employment Interruption

Taking a career break can also benefit your pension assets. When you leave a pension fund, your assets transfer to a vested benefits foundation. Depending on your break’s duration or future employment situation, it might be wise to keep your money there and consider investing it. A vested benefits custody account protects you from redistribution within the 2nd pillar and allows you to decide your investment strategy. With careful retirement planning, you can also save on taxes.

Redistribution – What is it?

Your monthly retirement capital in the pension fund is invested in financial markets, generating returns. However, these returns are partially used to finance existing retirement pensions. You will not notice this directly, but you can compare it with your pillar 3a, for example: Let’s assume that you have invested your pillar 3a assets in the stock market and thus achieve an annual return of CHF 300. In December, the bank decides to credit only CHF 150 to your account and uses the remaining CHF 150 for other purposes, including to cross-subsidize other customers.

This is exactly what happens in the 2nd pillar.

Part time Workload

If you’re considering or already working part-time, it’s vital to understand its impact on your insurance and pension provision. Here are some tips for making appropriate provisions for part-time work.

Entry Threshold & Coordination Deduction

Employees earning less than CHF 21,510 annually (CHF 1,792.50 per month) typically aren’t insured in the pension fund. Some employers adjust the entry threshold and coordination deduction based on employment level, which can improve your retirement and pension benefits.

More information and sample calculations are available hier.

Different Savings Rates & Benefits in the Event of Death and Disability

We distinguish between mandatory and non-mandatory benefits in the pension fund, including savings and risk components. The statutory savings contributions are:

25 – 34 years: 7%

35 – 44 years: 10%

45 – 54 years: 15%

55 – 64/65 years: 18%

For example, a 32-year-old with an insured annual salary of CHF 60,000 will save CHF 4,200 annually for retirement. Companies can voluntarily increase these rates, leading to higher monthly deductions but also a larger pension. Employers may also choose to fund a greater portion of these deductions.

The same principle applies to death and disability benefits, with employers having the option to increase statutory minimums.

As illustrated, your choices significantly affect your financial security now and in retirement. Major opportunities arise with job changes or extended work breaks. Therefore, examining your future employer’s pension fund benefits is crucial.

Take Control of Your Finances Today

How does this resonate with you?

Would you like to be informed once Melina Scheuber or her colleagues publish articles around pension fund and financial topics ?

Please sign up for our newsletter.

You are currently viewing a placeholder content from HubSpot. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More Information

[1] Fairplay Studie der Vita Sammelstiftung

* All figures in this article are as of 2022