Author: Melina Scheuber

The pension system can be complex, with many technical terms adding to the complexity of understanding occupational pensions. Here’s a simplified explanation of some key terms.

Coordination Deduction & Insured Salary

The coordination deduction helps align pensions between the first and second pillars, ensuring that the pension fund only charges contributions on the portion of your salary not already covered by the first pillar.

The deduction is 7/8 of the maximum AHV pension, currently CHF 25,095.

For example, if your annual gross salary is CHF 70,000, subtracting the coordination deduction of CHF 25,095 leaves a coordinated salary (or insured salary) of CHF 44,905.

Calculation Example: Effects of the Coordination Deduction

The 2nd pillar comprises a pension insurance component and a risk insurance component. Upon retirement, you receive a pension; in the event of risk (death or disability), cash benefits are paid to your spouse and children.

Your savings contributions (retirement credits) and risk contributions (insurance cover) are based on your insured salary. These combine to form the social security contributions deducted from your salary each month.

Thus, the coordination deduction impacts your insured salary, affecting how much you save for retirement and your insurance benefits in events like death or disability.

Entry Threshold

In Switzerland, employees are compulsorily insured in the pension fund against death and disability from January 1 of their 18th year and with a minimum income of CHF 21,510 (CHF 1,792.50 per month). From the 25th year, additional savings for retirement begin. Those earnings below this threshold are not connected to a pension fund and lack insurance in the 2nd pillar.

Effects of the Pension Fund Entry Threshold on Women

Pension Plans / Mandatory and Extra-Mandatory Plans

Pension funds have mandatory and extra-mandatory parts. Mandatory benefits, regulated by the state, are uniform across all pension funds and employers. The extra-mandatory part varies, as employers decide which pension and insurance benefits to offer. These can be uniform or vary based on different pension plans.

Example:

- Pension Plan 1: Commercial employees with salaries up to CHF 100,000

- Pension Plan 2: Managers with salaries up to CHF 200,000

- Pension Plan 3: Executive staff with salaries of CHF 200,000 or more

Benefits vary by plan, meaning different employers offer distinct advantages in terms of retirement capital and protection in disability cases.

Pay-as-You-Go System vs. Funded System

Unlike the 1st pillar’s pay-as-you-go system (where the working generation finances retirees), the 2nd pillar is a funded system, meaning you save your own retirement capital.

Conversion Rate

At normal retirement age, you receive a pension based on your saved retirement capital since age 25 and the conversion rate, currently 6.8% in the BVG mandatory scheme. In the BVG extra-mandatory scheme, conversion rates may differ.

For instance, with CHF 300,000 in your pension fund, you’d receive an annual pension of CHF 20,400 (6.8% of CHF 300,000) under the BVG mandatory scheme.

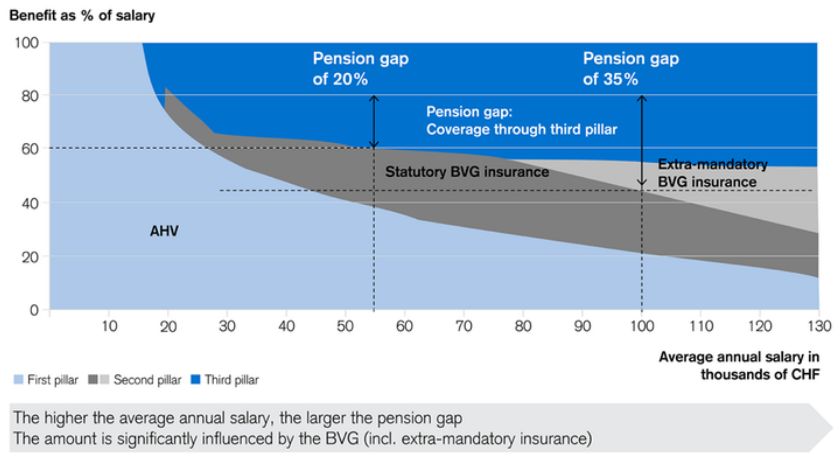

Pension Gaps

These occur if we’re unemployed for a period and don’t contribute to the pension fund. Reasons include parental leave or a stay abroad. High income can also cause gaps, as the first and second pillars cover a smaller proportion of high gross incomes, emphasizing the importance of the third pillar.

For example:

- CHF 80,000 salary yields approximately 60% pension (CHF 48,000) from the 1st and 2nd pillars.

- CHF 120,000 salary yields around 55% pension (CHF 66,000).

Pension gaps are listed on your annual pension fund statement as purchase potential, calculated based on your current salary and the hypothetical retirement capital you would have saved had you maintained this salary since age 25. Changes in employment can affect benefits and gaps. There is a high probability that your savings would be considerably higher today (unless you have a lower salary today than in the past). The difference to your actual savings amount is the purchase potential.

How we are insured in the pension fund depends on our employer. If we change our employer, our benefits and therefore our gaps or purchase potential may change again. It is important for you to know that you have a direct influence on your retirement and insurance benefits.

Women are particularly affected by retirement provision gaps, receiving about 37% less than men. Part-time work, career breaks for family or care, and lower salaries result in smaller pension contributions and less retirement money. These gaps aren’t quantified on pension fund statements.

Impact of Part-Time Work, Maternity Leave, and Pay Inequality for Women

Pension Fund Purchase

Many consider making voluntary pension fund contributions at year’s end. Your pension fund statement shows your purchase potential, which can be tax-deductible and is particularly beneficial after age 50.

Good Planning Pays Off – What to Consider When Buying into a Pension Fund

“WEF Advance Withdrawal” – Promotion of Home Ownership

You can withdraw some or all pension assets for home purchase or construction. Up to age 50, you can withdraw all retirement assets; restrictions apply afterward. Withdrawals are possible every five years, with a minimum of CHF 20,000. Consider additional insurance for death and disability as withdrawals reduce pension benefits.

Promotion of Home Ownership with Occupational Pension Funds

Redistribution – What Is It?

Your monthly retirement capital in the pension fund is invested, generating returns. However, not all returns are credited to you, as some finance existing pensions with a portion of the returns on your capital. You will not notice this directly, but you can compare it with your pillar 3a, for example: Let’s assume that you have invested your pillar 3a assets in the securities market and thus achieve an annual return of CHF 300. In December, the bank decides to credit only CHF 150 to your account and uses the remaining CHF 150 for other purposes, including to cross-subsidize other customers.

This is what happens in the 2nd pillar.

BVG 1e

This provision in the BVV 2 Pension Act allows higher-earning individuals to choose their investment strategies within the pension fund.

BVG 1e management plans, offered to employees earning over CHF 129,060, are part of the extra-mandatory scheme, providing greater self-determination in pension provision and reducing redistribution issues.

* All figures are gross values for 2022.

Take Control of Your Finances Today

How does this resonate with you?

Would you like to be informed once Melina Scheuber or her colleagues publish articles around pension fund and financial topics ?

Please sign up for our newsletter.

You are currently viewing a placeholder content from HubSpot. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More Information