Author: Melina Scheuber

Choosing between marriage and cohabitation is a deeply personal decision. While there’s no definitive right or wrong, understanding the financial and insurance implications is essential

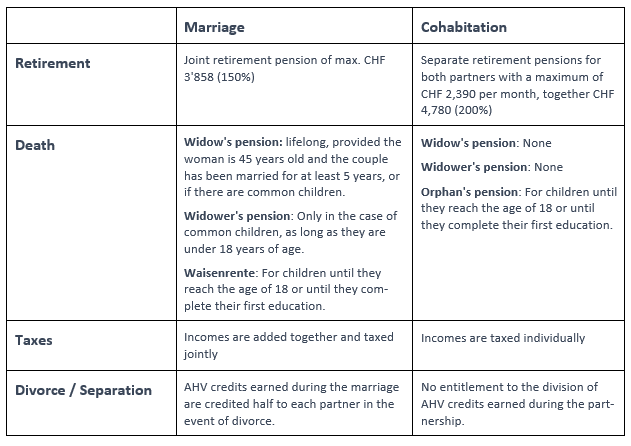

Pillar 1: Old-Age and Survivors’ Insurance (AHV/IV)

In marriage, a couple’s maximum AHV pension is CHF 3,585, 1.5 times the individual maximum. Additionally, the surviving spouse may be eligible for a widow’s or widower’s pension under certain conditions. AHV credits accumulated during marriage are equally split upon divorce (spousal splitting).

Cohabitants each receive a full individual retirement pension, totaling up to CHF 4,780, which is roughly 25% more than that of a married couple. However, they lack coverage for survivor’s pensions and cannot split AHV credits upon separation.

Pillar 2: Pension Fund (Occupational Benefits + Vested Benefits)

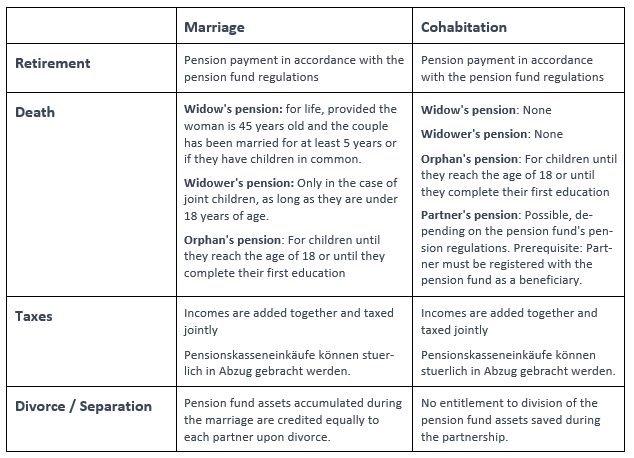

The retirement pension amount from the 2nd pillar is influenced by various factors, with no differences between married and cohabiting couples.

Differences arise in the context of death and the inheritance of vested benefit assets.

In marriage, the surviving spouse generally receives a survivor’s pension from either the accident insurance or the deceased partner’s pension fund. Like AHV, pension fund assets accrued during marriage are equally divided in case of divorce.

For cohabitants, there is no legal entitlement to survivor’s benefits from the 2nd pillar. However, many pension funds offer a partner’s pension under certain conditions. It’s important to register your cohabiting partner as a beneficiary with your pension fund to secure the partner’s pension in case of risk.

Vested Benefit Assets

In marriage, vested benefits are automatically paid out to the surviving spouse and descendants upon death.

Cohabitants can designate each other as beneficiaries for vested benefits in the event of death. It’s necessary to inform the vested benefits foundation about the beneficiary status and understand its requirements.

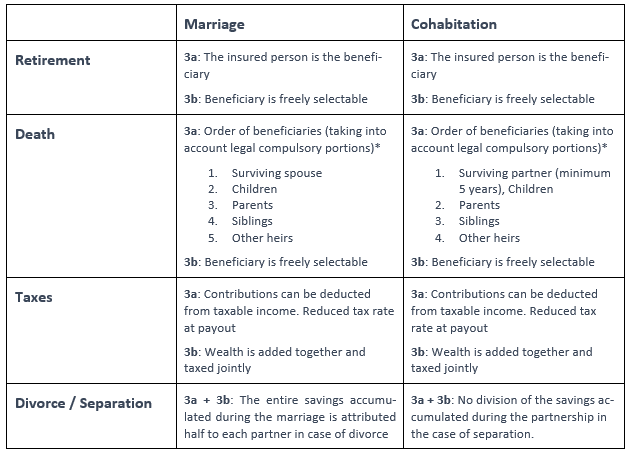

Pillar 3: Restricted (3a) and Unrestricted Pension Provision (3b)

In marriage, couples automatically benefit from Pillar 3a & b funds in case of a partner’s death or divorce. In death, statutory regulations dictate entitlement to the deceased’s assets. In divorce, half of the assets saved during marriage are credited to each partner.

Cohabitants can also benefit from Pillar 3a upon death through a will and notifying the Pillar 3a Foundation. Mandatory contributions must be considered if there is a spouse and/or children. Without a written agreement, cohabiting couples don’t automatically split assets saved during their relationship upon separation.

Additional Considerations

Inheritance Law

Switzerland recognizes three matrimonial property regimes: joint, separate, and community property. Without a different agreement, division of property applies upon marriage. This regime is fundamental for dividing or inheriting assets in divorce or death. The surviving spouse is always entitled to inheritance, the extent of which depends on the matrimonial regime, potential descendants, and any existing agreements like wills or inheritance contracts.

Cohabitants have no legal claim to the deceased partner’s assets. They can secure mutual benefits through written agreements such as wills, inheritance contracts, and designations in the second and third pillars.

The Cohabitation Contract

Cohabitation lacks legal regulation. Through a cohabitation agreement, unmarried couples can arrange and document aspects like household management, asset division, death protection, child custody, maintenance after separation, and more. The following topics can be defined in a cohabitation contract :

- Shared Household

What belongs to whom? How are the household costs and labour divided? Who stays in the home after a possible separation? How long does the partner moving out have to help pay the rent? - Assets

How will the assets be divided in the event of separation? - Protection in the event of death

How will the surviving partner be covered in the event of death? Do we take out death risk insurance? - Joint children

How will custody be arranged in the event of separation? Who pays how much maintenance? Does the stay-at-home partner receive a salary and if so, how much? - Separation

How high are the monthly maintenance contributions that the financially stronger partner pays to the economically weaker partner after a separation?

Advance Care Directive & Living Will

Recommended for all, these documents specify representation in incapacity (Advance Care Directive) and medical decisions when unable to communicate preferences (Living Will).

Powers of Attorney – Bank acoounts

These are invalid post-mortem. Hence, it’s advised that couples with joint accounts also maintain individual accounts to ensure financial access immediately after death.

Taking Control of Your Finances Married couples benefit from automatic financial provisions upon marriage. Cohabitants should consider a cohabitation agreement and designate beneficiaries in pension plans, vested benefits foundations, 3rd pillar, and life insurances. A will and/or inheritance contract can also help secure inheritance rights in cohabitation.

Take Control of Your Finances Today

How does this resonate with you?

Would you like to be informed once Melina Scheuber or her colleagues publish articles around pension fund and financial topics ?

Please sign up for our newsletter.

You are currently viewing a placeholder content from HubSpot. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More Information