Review and Outlook

The brave owns the world, the cautious the future.

The world of investors is and remains indestructible. Stock markets and investors are brimming with confidence, and quotations ignore every warning, no matter how clear. Rightly so, or is it inefficient?

The fact that the Nobel Prize for Economics in 2013 went to Eugene F. Fama, Lars Peter Hanson and Robert J. Shiller is evidence of the never-ending debate on stock market pricing and its irrationality. Are they now efficient, or does “irrational exuberance” exist?

A look at interest rates and the recent development of the stock markets seems to make this question obsolete; irrationality is often present. Those who doubt this conclusion may have been convinced by the oil market: Not only did the price of oil collapse, it actually slid deep into negative territory. Anyone who bought a one-month futures contract on WTI crude oil on 20 April, thus committing himself to receive the oil in May, was paid a whopping 40 dollars a barrel by the sellers. So there it is, the irrational exaggeration, as far as the eye can see.

However, this statement does not go far enough, as there are exaggerations in certain sub-sectors and in markets where intensive intervention is possible. By contrast, the markets as a whole – i.e. all asset classes combined as a basket – are developing in an orderly and controlled manner. This is an excellent argument for balanced, well-diversified portfolios that reflect this basket. Unfortunately, we are now seeing that this sensible approach has fewer and fewer followers; instead of diversification, the aim is extreme positioning to optimise returns. The bird in the hand is let out, because the two in the bush seem more attractive. However, such an investment strategy involves considerable risks.

| Asset class | Index | Return 3 months, as of 31.06.2020 in base currency | Return 12 months, as of 31.06.2020 in base currency |

|---|---|---|---|

| Equities World | MSCI World Net USD | 19.36% | 2.84% |

| Equities Switzerland | Swiss Performance Index | 9.86% | 3.83% |

| Equities EM | MSCI Emerging Markets NR USD | 18.08% | -9.78% |

| Bonds World | JPM GBI Global Traded TR USD | 1.46% | 5.24% |

| Bonds Switzerland | Swiss Bond Index AAA-BBB TR | 2.15% | -0.65% |

| Commodities | Thomson Reuters/Jefferies CRB TR USD | 13.33% | -22.81% |

| Real Estate Switzerland | SXI Real Estate® Funds TR CHF | 1.87% | 5.07% |

| Real Estate World | FTSE EPRA/NAREIT Global TR USD | 10.18% | -15.49% |

| Exchange rate EUR/CHF | 0.36% | -4.12% | |

| Exchange rate USD/CHF | -1.43% | -2.96% |

The central banks continue to cut interest rates. Whatever their reasons are for doing so, one thing is clear: this does not solve the problems, but rather postpones them into the future, thereby exacerbating them if anything. It is also striking that central banks around the world are reacting from a defensive position and justifying their decisions – and not the other way around. Central banks quite simply take the path of least resistance when they are prepared to experiment because governments are breathing down their necks and threatening them. Where aid is forced and unavoidable due to mismanagement, market pricing starts to produce strange blossoms. Exaggerations emerge to the point of irrationality. This development can of course last for a long time, but its end is inevitable. The return to reality is often a quick and extremely painful process.

However, since in 2013 not only one Nobel Prize winner was awarded, there is also Fama’s market efficiency hypothesis in addition to Shiller’s theory of “irrational exaggerations”. It states that market participants behave rationally and that markets are in equilibrium at all times. Is this theory completely absurd, or is there a hint of truth in it?

The markets can best be compared to a mobile that commutes smoothly and quietly back and forth as long as the window is not opened. Sometimes one element is in the foreground, sometimes the other. All asset classes are in constant motion, and their prices dance around an imaginary middle. At the moment, however, the window is wide open; the restlessness is clearly noticeable. What is still missing is the draft that could create the final mess. But we are on the way to doing so, and the trade war between the US and China is one of the signs.

Risk Regime Investing (RRI) Outlook

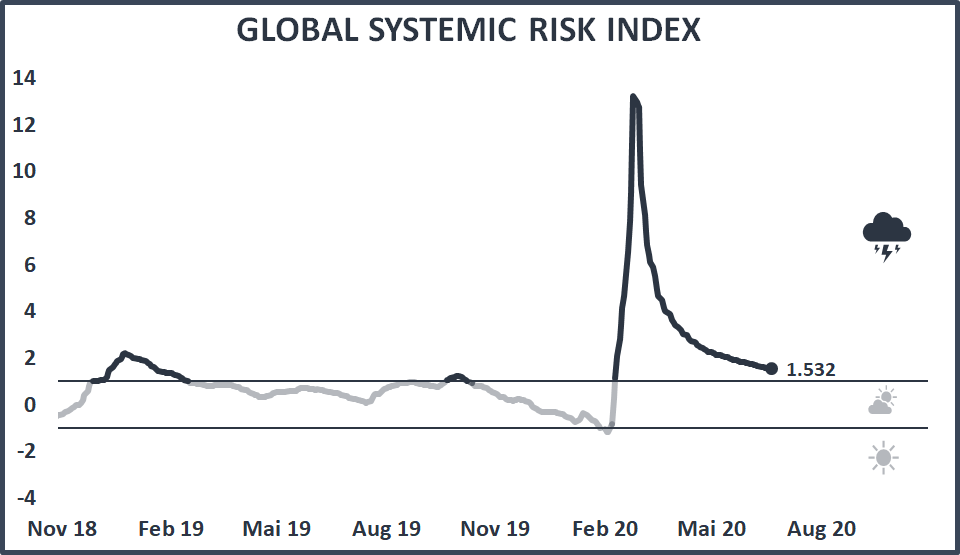

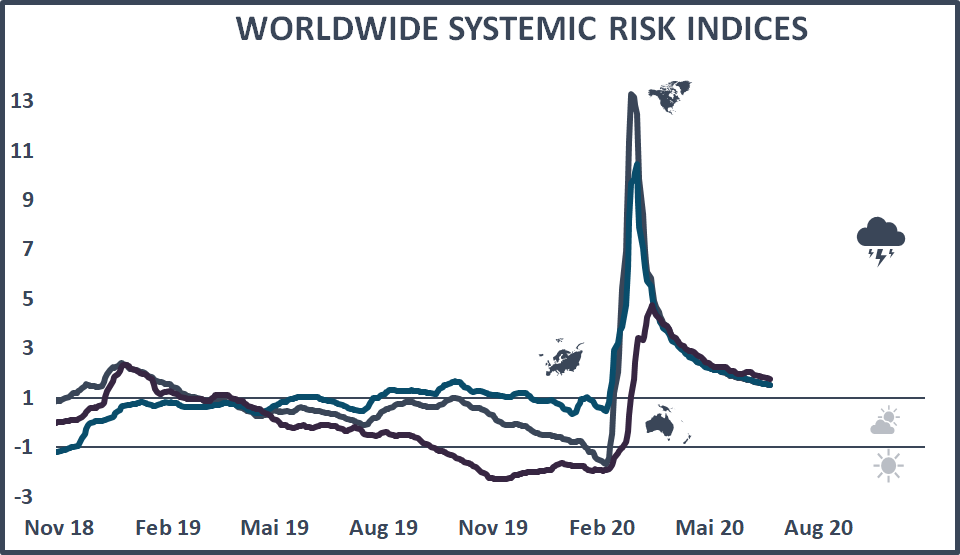

Most important first: Our Global Systemic Risk Index has declined significantly over the last four months. However, the warning signs have not disappeared despite the recovery in the markets. The risk concentration observed with the index remains significant, and the situation in the asset markets is extremely fragile worldwide.

It is once again time to face the manifold problems. Be it the Covid-19 crisis, the geopolitical tensions, the trade war, the desolate leadership of the US, the helicopter money, the looming recession, the debt levels, global warming, or the unique counteraction of the monetary authorities. All of these inconsistencies seem to have no effect on the stock markets. But the question is not “why”, but “how much longer”.

It is also worth mentioning that, following the Japanese and European central banks, since this spring the US Federal Reserve has also committed itself to a policy of zero interest rates – a significant change in the global investment landscape that has given a great boost to all tangible assets.

If one classifies the above problem areas, the following main drivers for the above-mentioned risk concentration emerge:

- the Covid 19 crisis and its aftereffects

- the asset inflation and its consequences

- the changes in the geopolitical landscape brought about by the US

Now we come to the most important topic of these days, the development of the USA – the most important economy of the last decades. What is currently happening with and in the United States? Where is the threat of the US becoming detached from the other major economies leading to?

It is now definitely obvious that the idea of the founding fathers of the USA is no longer shared by large parts of the population. The epitome of freedom and unlimited possibilities, as it is almost pathologically celebrated in the USA, is more of an illusion than a reality. Why is the American society so deeply divided?

Life in the supposedly most liberal country in the world has become unaffordable for many Americans. The welfare state driven to excess celebrates the successful and forgets those in need. That would work if the successful were the majority. But that is not the case; it is a minority, an elite. One consequence of this development is that the population of entire regions enjoys hardly any medical care and is dependent on humanitarian organisations and voluntary helpers (doctors, surgeons, dentists, nurses) for health services. The USA is a highly developed country that is primarily geared towards maximum productivity and generates severe inefficiency on the fringes of society. And Covid-19 shows the weaknesses of these highly developed structures. Supply chains that are geared towards “just in time” are disintegrating. Basic products and know-how are missing because activities have long since been efficiently outsourced. The dangers of this approach grow exponentially with change; short-term fine-tuning is not possible, but often requires a change of system because the entire value chain is affected.

«Hire and fire» may lead to better quarterly results, but it leaves the strategically optimal path, with irreversible consequences. As a way out of the disaster, the world must then be threatened again – the long successful mechanisms of repression cast their long shadow. The world has learned, however, and the USA has gone way beyond the curve. Now the years could come when this policy will take its toll. And this price could become unbearable for the US and the rest of the world.

Stephen Roach of Yale University warns of a dollar crash with immeasurable consequences for the global economy, at best comparable to the stagflation of the 1970s, when prices (especially oil prices) rose sharply and the economy floundered. Are investors anticipating such a scenario with their actions, which are ultimately reflected in our Global Systemic Risk Index? Time will tell.

Quantitative Stock Selection (QSS) Outlook

Our Quantitative Stock Selection approach has more than proven itself in recent months. Despite extremely volatile markets and increased rotation in various dimensions, the results of our mandates are extremely close to their benchmark. Investors’ preferences change frequently, and cheap stocks are replacing overpriced internet stocks and, shortly afterwards, traditional financial stocks are at the top of the investors’ rankings. Nevertheless, we can state that QSS mandates are significantly more stable than the market – this despite the fact that our portfolios consist of a few selected securities, which are nevertheless very well diversified.

The QSS approach is suitable for making an efficient and effective stock selection from any universe according to objective criteria. This is a selection procedure common to traditional indices, and one that every investment advisor strives to follow. However, if this selection process is to be carried out across all dimensions of professional company and stock analysis, the volume of data to be processed quickly exceeds the capacity of investment advisors. The selection process is therefore often driven by preferences rather than facts, and fails at least in some areas.

Our Quantitative Stock Selection is also suitable for very specific universes and indices which, for example, cover ESG factors (Environmental, Social, Governance) or the character “Disruptive Industries” (as the following example shows).

How do we manage your individual «portfolio of the future» with the QSS approach?

In a first step you can choose your preferred topics or technologies from a variety of «Disruptive Industries». These include robotics, clean energy, autonomous mobility, artificial intelligence, smart home, space travel, drones, cyber security, nanotechnology, virtual reality, genetics, clean technologies, digital networks, alternative finance, 3D printers, block chain technologies, new payment platforms, democratized banking, advanced logistics, and many more. As a basis for the various industries, we use an index family built according to a proven index methodology that captures the components and drivers of the fourth industrial revolution. The assessment of which of these industries offers the greatest potential is highly individual. We therefore leave this selection to our clients, you, but are at your side to advise you as required.

With our QSS approach, the representatives of the selected (for example five) “Disruptive Industries” can now be defined as a universe. This includes, for example, 150 stocks from which we select the best stocks based on objective criteria so that all five themes are equally represented in your individual portfolio. The portfolio compiled in this way thus contains, for example, the four most promising titles of the selected future industries, i.e. a total of 20 titles.

The QSS selection process and investment approach ensures that the selected securities are continuously monitored for their economic performance and replaced if necessary.

We are pleased to be at your disposal for discussing your “Disruptive Industries” selection and for structuring your individual future portfolio.

Global Financial Markets – Review

Equities

We wrote about the first quarter of 2020 that investors would not forget it so quickly. This statement also applies to the second quarter – albeit in reverse. In a volatile environment, the international stock markets achieved high gains and made up some of the first-quarter losses; fuelled by the increasingly expansive monetary policy of the central banks and detached from economic reality. The MSCI World index closed the quarter with an impressive gain of 19.36%, while emerging market equities, as measured by the MSCI Emerging Markets index, advanced 18.08%. The SPI gained 9.86% between April and June, lagging behind other European exchanges and the United States. Investors denominated in Swiss francs suffered smaller currency losses in dollar-denominated securities.

Bonds

Investment grade bonds were the only asset class to finish the first quarter of 2020 in the positive zone. They continued this trend and also showed a slightly positive performance in the second quarter. JP Morgan’s globally invested index rose 1.46% from April to June, which is equivalent to a performance of -0.64% in Swiss francs. Swiss franc bonds with a credit rating between BBB and AAA yielded 2.15% in the second quarter. The difference in yield between short- and long-term Swiss franc bonds narrowed slightly in the second quarter.

Commodities

Commodity prices, which plummeted in the first quarter, were also able to recover a smaller part of the losses. The oil market stabilised after record low negative prices were demanded on 20th April – triggered by expectations of a massive slump in global demand as a result of the corona crisis and power politics games in Saudi Arabia. In June, a barrel of WTI crude oil again cost around 40 dollars, around a third less than at the beginning of the year. The broad-based commodity index CRB rose 13.33% in the second quarter (10.99% in Swiss francs). Gold lived up to its safe haven status in the second quarter, gaining 12%, up more than 16% since the beginning of the year.

Real Estate

Securities invested in real estate were also dragged down by the market slump in the first quarter, and the real estate markets came to an abrupt halt after an excellent 2019. Swiss real estate measured by the SXI Real Estate Funds recovered somewhat from April to June, advancing a modest 1.87%. Foreign real estate investments rose 10.8% (7.9% in Swiss francs), against the backdrop of a 30% price slump in the first quarter. The situation for commercial real estate is likely to remain difficult and suffer from the consequences and structural changes brought about by the Covid 19 pandemic.

Currencies

In March, the world’s central banks flooded the markets with liquidity, the Fed cut interest rates to zero and the ECB took unprecedented action. These stabilised the financial markets, but the dollar suffered some significant losses; the greenback lost 1.43% against the franc in the second quarter. After a prolonged period of weakness, the euro recovered slightly and was 0.36% higher against the franc at the end of June than at the end of March. The single currency gained 1.83% against the dollar.