Author: Lucas Widmer

After extensive debate, Parliament has passed a bill to reform the BVG (Occupational Pension Provision). This article examines the reform’s impact on employees and companies and what the future holds.

5-Point-Plan[1]

1. Reduction of the Conversion Rate from 6.8% auf 6.0%

The most contentious change is the reduction of the pension conversion rate from 6.8% to 6.0%. This change affects future retirees, while current retirees will continue receiving their existing payouts. The current rate is economically unsustainable, leading to retirement losses borne by active insured individuals, effectively reducing their future pensions. This unintended redistribution is a significant concern (as explained by Swiss TV station SRF on redistribution in the BVG). By 2030, with around 1 million new pensioners in Switzerland, a reduced conversion rate will provide some relief, though it is still economically high.

2. Lifelong Pension Supplement for the Transitional Generation

To compensate for the lower conversion rate, a transitional generation of 15 cohorts will receive lifelong pension supplements based on retirement capital. Full supplements are for those with retirement assets up to CHF 215,100; degressive support is for assets between CHF 215,100 and CHF 430,200.

Implementation details remain unclear due to various practical considerations. Critics note that 50% of people in the transitional generation will receive supplements, though only 10-20% are affected by the rate reduction. This overcompensation will cost about CHF 11 billion.

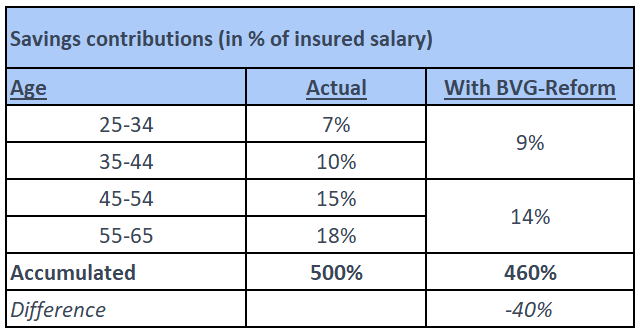

3. Adjustment of the Savings Scale

Annual savings contributions are also being adjusted. Rates for older employees will decrease, while younger employees under 35 will see higher savings credits. The intention is to reduce the cost burden of older employees. However, the reform will result in lower overall contributions:

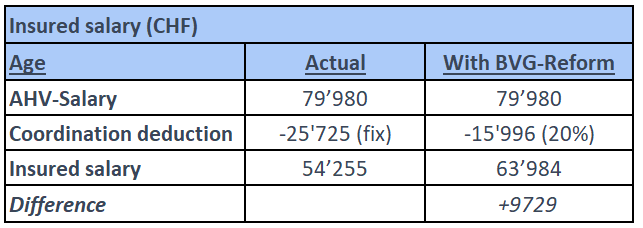

4. Flexibilization/Reduction of the Coordination Deduction

Many companies have already adjusted the coordination deduction for part-time employees. Now, it will be mandatory, making it 20% of the salary or a maximum of CHF 17,640. This change will significantly increase the insured salary in the 2nd pillar, depending on the initial situation:

5. Lowering the Entry Threshold

The new entry threshold will be CHF 19,845 (currently CHF 22,050), thus giving more people with low salaries access to a pension fund. As the coordination deduction in this salary range will be reduced the most in relative terms, these people will experience the greatest financial impact. The good news is that their pension provision will be massively strengthened. The downside is that this will significantly reduce the net salary paid out, as employees will also pay BVG contributions for savings, risk and administration.

Effects for Employees and Companies

The adopted measures will trigger various changes affecting employees and employers:

Employees

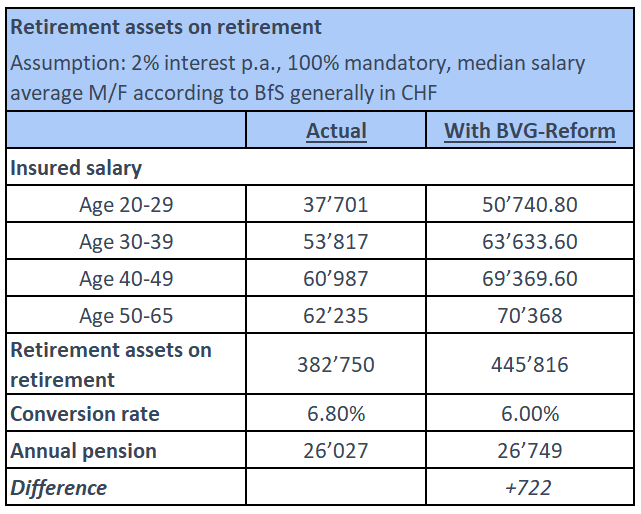

The table below compares the effects of the proposed BVG reform on the retirement assets of an employed person with the status quo, taking into account salary trends in the various age categories and assuming an average interest rate of 2% per year, which corresponds to the average of the largest collective foundations over recent years:

Projected retirement assets will be higher than under current legislation, despite lower cumulative contributions from Table 1. Higher insured salaries and contributions in younger years, combined with the compound interest effect, compensate for lower rates and conversion rates at older ages. Lump-sum beneficiaries can expect 16% higher pension assets.

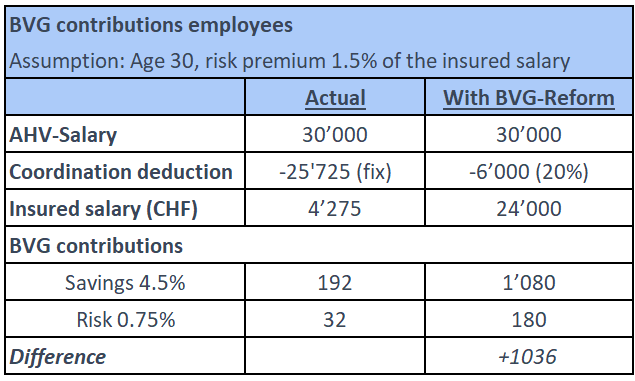

The amount of contributions and therefore the net salary paid out will also change drastically for people on low wages and part-time employees because the coordination deduction will be greatly reduced:

Effects for employers

On the company side, the BVG reform contains changes that can have a significant financial impact. In particular, companies with part-time employees, young staff and lower salary structures will be faced with significantly higher savings and risk contributions for the BVG, as shown in Table 4. Our pension experts will be happy to model the effects for your company and draw up proposals for action.

Our Initial Conclusion on the BVG Reform

From today’s perspective, it is uncertain whether the reform will come into force at all. The left-wing political camp has already announced that it will hold a referendum, meaning that the people will have the final say. The referendum deadline is July 6, 2023 [3]. If you think back to the referendum campaign and result on the 1st pillar last fall, doubts arise as to whether Swiss voters will approve this law. A “no” at the ballot box is likely to have serious consequences for the entire 3-pillar system and set the discussion back many years.

Even if the proposal in no way solves the problems of the BVG, it will bring relief. On the positive side, the excessive conversion rate will be reduced, the expected retirement assets of employees will increase in many cases and part-time employees in particular will be able to close pension gaps.

At the same time, it is a missed opportunity to tackle redistribution in the long term. The new conversion rate of 6% is still too high. At the same time, the compensation payments are financed by the active insured and fixed at the same time, which ensures that redistribution will continue for many years to come. Our call for personal responsibility in pension provision has proven its worth and will also pay off in the medium to long term.

Take Control of Your BVG Today

How does this resonate with you?

Would you like to be informed once Lucas Widmer or his colleagues publish articles around pension fund and financial topics?

Please sign up for our newsletter.

You are currently viewing a placeholder content from HubSpot. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More Information[1] Final Vote Text of the BVG Reform

[2] Federal Statistical Office, Gross Monthly Salary by Age and Gender, 2020

[3] Vorsorgeforum.ch: BVG Reform Referendum until July 6