Author: Lucas Widmer

In Arlesheim, a gastronomy and fine food entrepreneur demonstrates how to reform a personal pension fund solution independently of politics.

Three Employees Fall Through the Cracks

Occupational pension provision at the statutory minimum presents financial challenges not only for pension funds but also for employees of Swiss companies. The owner of the 300-year-old Gasthof zum Ochsen and the associated Jenzer butcher’s shop in Arlesheim became aware of this through three employees in different circumstances. They exemplify the pitfalls of pension fund solutions based on the statutory minimum, prevalent in many companies:

You are currently viewing a placeholder content from Default. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

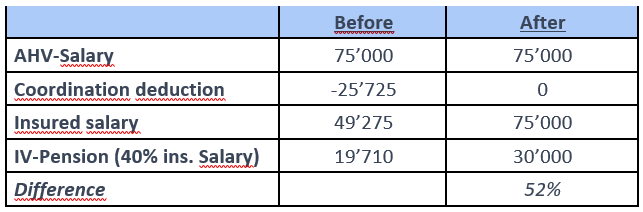

Disability: Financial Struggles Alongside Health Issues

One employee’s situation made Christoph Jenzer aware that the adjustment was overdue. Following an accident, he became reliant on a disability pension. With an average salary in the food industry, this equates to a BVG disability pension of CHF 19,710 per year or CHF 1,642.50 per month with the old pension plan at the GastroSocial Pension Fund – a situation described by owner Christoph Jenzer as “catastrophic”:

The situation after the adjustments made (“After” column, more details in the next section) improves significantly. A pension from the 1st pillar and from accident insurance must be added if an accident was the cause. Nowadays, however, around half of all cases of disability are due to illness (e.g. mental illness). These are not covered by accident insurance and are therefore significantly less financially secure.

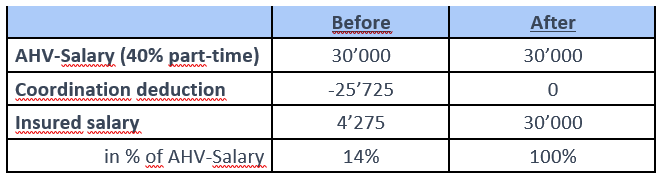

Part-time work: fraction of salary insured in pension fund

Another problem typical of the BVG that Christoph Jenzer mentions is that of part-time employees. If the coordination deduction is not adjusted to the level of employment, a much smaller proportion of the salary is insured in the pension fund than is the case for full-time employees. As a result, just one seventh of the salary of a part-time employee with a 40% workload is insured in the pension fund:

People who earn less than CHF 22,050 per year from an employer with a full coordination deduction (e.g. because they work a low salary of between 20-40%) are even excluded from the pension fund altogether as they fall below the entry threshold.

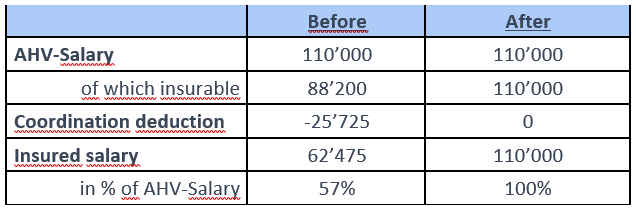

BVG minimum: Insured Salary Limitation

The third problem tackled by the Arlesheim entrepreneur involved a management employee insured for only a fraction of his salary due to the maximum insurable AHV salary limit of CHF 88,200 (minus coordination deduction). This resulted in significant retirement savings gaps:

Small Changes, Big Impact

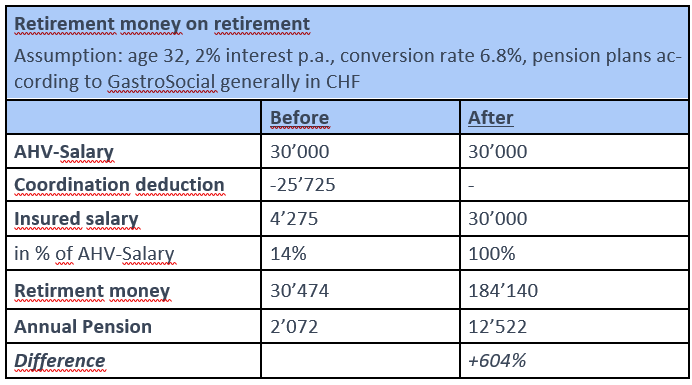

The reasons for these coverage deficiencies trace back to two legal parameters: the coordination deduction and the insured salary limit. By switching from the GastroSocial “Uno Basis” to “Uno Integral Top”, employees can anticipate improved risk protection and up to six times higher pensions upon retirement. The example of the part-time employee, assuming a 32-year-old at the time of adjustment, illustrates this:

Assuming that the person is 32 years old at the time of the adjustments, the projected retirement pension increases by 604% compared to the old model, with all other conditions remaining the same. The new amount of around CHF 1,000 per month that can be expected is also “not a bequest, but a good solution for everyone”, as the owner notes.

Of course, these improvements also entail certain costs. The additional contributions of CHF 150 per month and employee (CHF 170,000 per year for the entire workforce) must be earned. From Christoph Jenzer’s point of view, this investment in employees is worthwhile, as it boosts motivation and at the same time makes the company more attractive as an employer.

How you too can reform your pension fund

As Christoph Jenzer emphasizes, such positive changes to the pension fund are very well received by employees. In addition to the measures taken by Metzgerei Jenzer, there are other ways to improve the occupational benefits of your own employees. Before tackling these, it is advisable to draw up an overview of the current pension plans and compare them with competitors. Parsumo offers companies with 100 or more employees a comprehensive pension plan benchmarking service for this purpose. Get in touch with us and arrange a non-binding initial consultation.

Sources:

SRF Beitrag

PENSO Magazin 03/2023

GastroSocial Blogartikel

Salarium

PENSO Magazin 03/2023

BSV IV-Statistik 2020